Tax burden per inhabitant in Albania, 2022

According to Report TB 2023, The tax burden is the product of the revenues collected by the central tax administration and the customs administration, from the revenues from the local government, as well as the receipts for social and health insurance contributions constitute the comprehensive part that is calculated in relation to the number of residents of the districts in 2022 [1].

The tax burden from taxes and customs has a performance increase of 15.6% in 2022 compared to the previous year. In 2022, the strengthening of tax administration, as well as the impact of inflation and the maintenance of prices of energy products and frozen foods led to better performance levels for the budget, but with an increase in the tax burden on taxpayers.

The burden of social and health insurance contributions has an increasing performance of 10.8% in 2022 compared to 2021. The weight of the contribution burden in the structure of the tax burden has decreased in 2022 by 0.7 percentage points less than in 2021.

In the analysis of the tax burden according to the calculation methodology, it results that the average tax burden for Albania is 141.4 thousand ALL per year per inhabitant.

The tax burden distributed on average during the year for Albania is 11.8 thousand ALL per month for each resident.

The tax burden from taxes and customs has a performance increase of 15.6% in 2022 compared to the previous year. In 2022, the strengthening of tax administration, as well as the impact of inflation and the maintenance of prices of energy products and frozen foods led to better performance levels for the budget, but with an increase in the tax burden on taxpayers.

The burden of social and health insurance contributions has an increasing performance of 10.8% in 2022 compared to 2021. The weight of the contribution burden in the structure of the tax burden has decreased in 2022 by 0.7 percentage points less than in 2021.

In the analysis of the tax burden according to the calculation methodology, it results that the average tax burden for Albania is 141.4 thousand ALL per year per inhabitant.

The tax burden distributed on average during the year for Albania is 11.8 thousand ALL per month for each resident.

This burden includes the VAT that each buyer pays for goods and services, for beverages and fuel that each consumer pays, for the tax on wages that each employee pays, the payments of profit tax from businesses, for the capital tax that each individual pays receives income from rent, from bank interest, from the sale of movable and immovable property, from intellectual property, from dividends, household payments for local taxes and fees, payments of social and health insurance contributions, customs fees and duties, national taxes and other tax obligations, which are not mentioned by name as above.

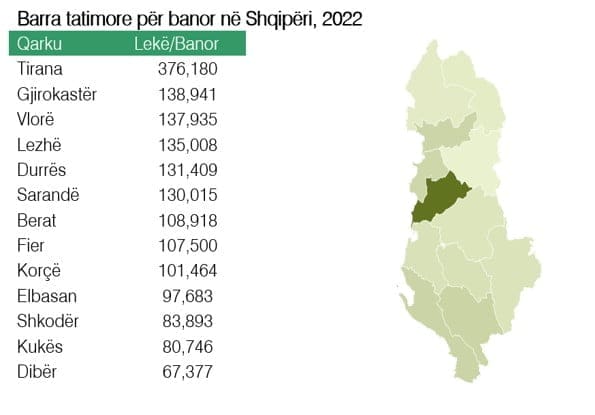

In the analysis of the tax burden according to the largest municipalities that include several municipalities within the district, it results that the highest level is in Tirana, where on average each resident paid 376.2 thousand ALL in 2022 during their daily life.

All other municipalities of the country have a burden less than half of the tax burden of Tirana’s residents, but even below the average level of the country’s tax burden.

Gjirokastra is the second for the total tax burden, where on average each resident paid 138.9 thousand ALL in 2022.

Next comes the region of Vlora (without Saranda), where the calculation shows that on average each resident paid 137.9 thousand ALL in 2022.

In the following, as it results in the ranking in the chart above, Lezha comes with 135 thousand ALL per year, Durrës with an average annual tax burden of 131.4 thousand ALL, Saranda with 130 thousand ALL per year, Berati with 108.9 thousand ALL per year, Fieri with 107.5 thousand ALL per year, Korça with 101.4 thousand ALL per year.

Meanwhile, the tax burden in Elbasan on average is 97.7 thousand ALL per year per resident, in Shkodër it is 83.9 thousand ALL per resident per year, in Kukës it is 80.7 thousand ALL per resident per year and the burden with the lowest level is in Dibër with 67.7 thousand lek per inhabitant per year.

Tax burden in relation to domestic production

Another measurement of the tax burden can be calculated in the weight that each municipality carries with the tax burden in relation to the Gross Domestic Product in 2022 (preliminary).

The weight of the regional tax burden (central and local taxes and duties) to the domestic production includes the calculation of the taxes paid to the state budget by each district to the country’s GDP. This income category includes tax burdens borne by taxpayers on behalf of the central tax administration (General Directorate of Taxes), as well as local tax administrations (Municipalities and units) plus social and health insurance contributions

The tax burden for all counties in 2022 weighs as much as 26.3% of GDP. The main weight, according to the value that goes to the state budget, is from the region of Tirana with a fiscal contribution of 16.4% of the country’s GDP, followed by Durrës with a fiscal contribution of 1.9% of the GDP.

The region of Fier makes a fiscal contribution to the state budget with a weight of 1.5% of GDP.

Then in fourth place is Elbasan with a fiscal contribution of 1.2% of GDP, Vlora with a fiscal contribution of 1.2% of GDP (slightly smaller than Elbasan) and Korça with a fiscal contribution of 1% of GDP. of the country.

The other regions have a fiscal contribution to the 2022 state budget together amounting to 3.2% of the country’s GDP.

Burden of consumption taxes and assessment of differences between regions

Kukësi has the lowest fiscal contribution to the budget at 0.3% of the country’s GDP.

For a more complete clarification of the tax burden of consumption taxes (VAT and Excise duty) in 2022 (the year with the highest inflation in recent decades), from the calculations made regarding the payment of VAT and excise duty in the state budget to total tax burden per inhabitant, it is observed that there is a situation with a difference in the ranking of the country’s regions compared to their ranking for the tax burden per inhabitant.

Thus, the tax burden per inhabitant is Tirana, but in fact the highest burden per inhabitant for consumption taxes is found in Saranda, where 56.9% of the tax burden of the inhabitants consists of the burden of VAT and excise duty, which represents the value of goods and services that they bought in 2022. Below we see that this ratio of VAT and excise duty to tax burden per inhabitant is high in Kukës, Elbasan, Dibër, Lezhë, Korçë and Vlorë. Meanwhile, in Tirana, Shkodër, Durrës, Gjirokastër, Fier and Berat, the burden of VAT and excise duty is below the 50% level in relation to the tax burden.

Notice! This fact is also worth looking at in comparison with the impact of consumer goods and services that are used more by visitors who move through the cities in Albania, affecting consumption, the amount of VAT that is part of the value of their expenses, also affecting the increase in burden resulting from this calculation.

An influencing factor is related to the distribution of goods and services for consumption, which tend to be consumed outside the area where they are created or produced for export or in densely populated areas.

These indicators are valid for transparency regarding the weight they carry with their payments for the direct budget, as consumers, but also businesses, investors and citizens, realizing that the downward trend of the weight of indirect taxes (pressure on consumer prices) and the increasing trend of direct taxes (impact on corporate profit and personal income) reflect the positive effects of the government’s fiscal policy, which aims at a redistribution of income by benefiting more from taxes on capital gains.

The ratio of the taxes paid or of the territorial unit within the country in relation to the GDP is an indicator that is valid to see how much the real contribution of taxpayers is. On the other hand, it is used to understand how much should be claimed to benefit back in the form of expenses that are made from the budget for services that are of great public interest.

On the other hand, a better local fiscal administration should justify the narrowing of the differences between the consumption and distribution of the population and businesses in the county.

Local tax burden and weight per inhabitant

Legal changes in the fiscal system (Fiscal Package 2022), on the one hand, aim to facilitate small business, the self-employed, but also distribute the tax burden more harmoniously between those taxed by labor and those taxed by capital. On the other hand, fiscal policy changes tend to normalize the situation in many sectors of the local economy. These changes, at the same time, increase the income in some municipalities where the benefit is greater for the main ones, e.g. Tirana Municipality, making it possible to provide more services with a higher quality.

Among the easing fiscal policies in the last two years in terms of local tax burden is the “Simplified Profit Tax” for small businesses, which has been abolished for the category of businesses with a turnover of 0 to 5 million ALL per year. However, the increase in the threshold of the annual turnover up to 14 million lek per year for the other category of businesses that tax the profit at 5% per year is another shift of the burden of this tax towards businesses that earn more, thus facilitating small business and especially the self-employed. The business with an annual turnover of 8 million to 14 million ALL, which is the change in the fiscal package, constitutes 20% of the number of businesses in the country.

In all 12 regions, more than half of the fiscal revenue consists of the fiscal burden collected from the citizens of the main district municipality.

Regions such as Tirana and Vlora have the highest tax burden per inhabitant in 2022.

Meanwhile, regions such as Shkodra, Lezha, Kukësi and Dibra carry the lowest tax burden. While the municipality of Saranda, with its specificity in the country’s tourism, carries a high burden in relation to the regions.

The local tax burden is seen to be no less than 3% of the total tax burden paid by each resident, as seen in Dibër, and no more than 9.9% of the total tax burden paid by each resident seen in Saranda.

The weight of the burden of local taxes and fees at the national level is on average 1/20 of the total tax burden, as presented above.

From the calculations of tax and fee payments according to municipalities, it is observed that close to 60% of the entire burden of local taxes, taxes and fees at the country level is borne by the citizens of Tirana.

The regions of Durrës, Vlora, Korça, Elbasan and Fier together (28 municipalities) carry a burden of 28% of the national local tax burden.

The remaining share of the local tax burden (12% of the total) is held by 31, mostly medium and small municipalities.

The disproportion of the tax burden also shows the debatable part of the administrative division and the open discussion on the financial productivity of the local finances of these municipalities.

The specific weight occupied by the counties of the country has specifics that include the number of taxpayers bearing the tax burden, industrial characteristics, gender compositions, population structure, education, natural resources underground and above ground, individual inherited wealth and assets created over two decades. , as well as elements of the environment and investments with public and private funds, including regional development plans.

These reports also guide the distribution of the segmentation of taxpayers, according to their size (micro, small, medium, or large).

From the data of the reports, the tax burden in the regions is kept at the quantitative level by the base of resident taxpayers that are included in the categories of micro (self-employed) and small businesses, than by the base of resident taxpayers that are included in the categories of businesses medium and large.

[1] https://www.instat.gov.al/media/9828/popullsia-me-1-janar-2022_final-15-04-2022.pdf

Leave a Reply

You must be logged in to post a comment.