Peace or disguised fiscal amnesty?!

Today, we want to share with you an in-depth analysis of a draft law making waves in Albania: the “Fiscal Peace Agreement.”

This proposal aims to “normalize” relations between the tax administration and taxpayers but raises serious questions about fiscal fairness, transparency, and alignment with European standards.

Based on a realistic and critical review, let’s dive into the details. This post isn’t just a summary, it’s a call to reflect on the long-term consequences of such policies.

The draft law proposes a voluntary agreement between taxpayers and the tax administration, lasting one year (extendable up to two years).

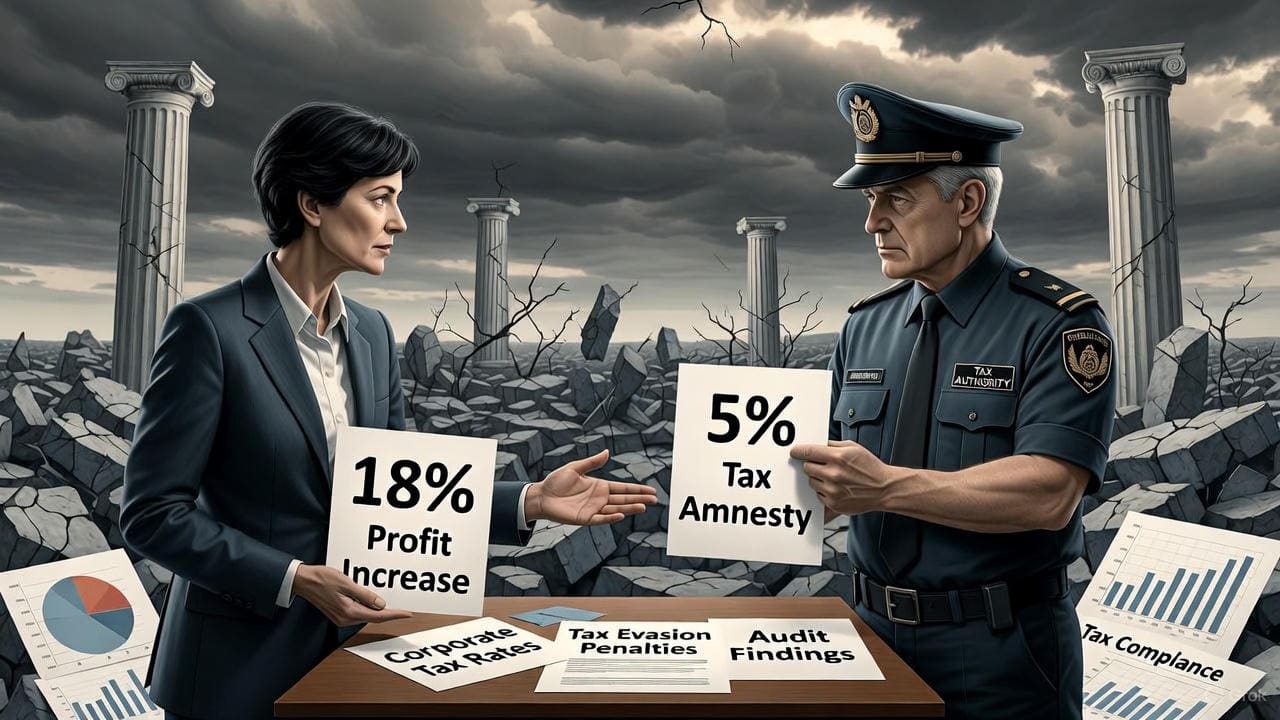

In exchange for declaring a profit increased by 18% compared to the previous year, businesses receive a guarantee of no tax audits during that period.

Additionally, it allows redeclaration of financial statements for the past five years, with a flat 5% tax.

At first glance, this seems like a pragmatic solution to reduce conflicts and boost budget revenues. But in essence, this is a tax amnesty by another name, a retroactive legalization of past financial inaccuracies with minimal penalties.

Is this true “peace,” or merely a postponement of deeper issues?

Let’s start with the potential upsides.

The law could create a conflict-free channel for resolving fiscal disputes, reducing administrative costs.

It offers a “fiscal ceasefire” between businesses and the state, injecting immediate cash into the budget via the 5% tax and the 18% tax base increase.

However, these benefits are illusory and short-lived.

In practice, the law replaces real tax control with administrative agreements, undermining fiscal fairness. It creates moral hazard: businesses that evaded proper declarations now benefit from soft legalization with minimal penalties. It institutionalizes informality, allowing entities to “clean” their records for five years at a symbolic 5% cost.

Imagine: a company that hid income can now sanitize its books for half a decade with just 5% tax. That’s not justice—it’s rewarding wrongdoing!

One of the biggest flaws is the violation of tax equality.

Under constitutional and universal principles, all taxpayers must be treated equally. Yet this draft does the opposite: honest businesses that paid correctly get nothing. Evaders gain audit immunity and legalization of discrepancies.

This sets a dangerous precedent.

Why comply regularly if you know an “amnesty” comes every few years?

It creates a vicious cycle where compliance is punished, not rewarded.

Albania aspires to EU membership, but this law clashes with the acquis communautaire, especially Chapter 16: Taxation.

The EU demands transparency, tax cooperation, and strong auditing, not ad-hoc deals that reduce oversight.

Instead of strengthening inter-administrative communication and audits, the draft promotes pre-set self-declaration, eroding system credibility. International partners may view this as a disguised amnesty, risking aid and negotiations.

Taxation should be based on actual, verified profits, not negotiated projections. A fixed 18% increase ignores industry capacities, economic cycles, and market structural changes.

For declining or recovering sectors, this becomes an unequal burden, encouraging artificial reporting to maintain agreement status.

This is a step backward in fiscal principles, making taxation subjective instead of objective.

Article 6 is the core problem, it allows redeclaration of cash inflows, long-term assets, liabilities, retained earnings, and dividends for the past five years, with 5% flat tax and no administrative penalties.

This enables cleaning falsified accounts, exempting auditors from liability, and using partner liabilities for personal asset formalization, a backdoor to laundering private wealth.

In effect, this replaces control and auditing with self-amnesty. Will this work without abuse?

The law severely limits the General Directorate of Taxes (DPT): field audits prohibited (except criminal cases), administration reduced to formal monitoring, and it creates a hybrid dependency between taxpayer and authority, a mix of contract and legal obligation.

This model weakens DPT credibility and risks turning fiscal relations into personalized negotiations.

In the short-term, there is a revenue boost from 5% tax + 18% base increase. In the medium-term, real revenue decline due to distorted tax base and falling compliance. In the long-term, expectation of new “fiscal peaces” every 3–4 years, eroding system trust.

Politically, the draft may serve as an electoral tool, favoring large businesses and easing audit pressure during election cycles.

But is the cost worth it?

The assessment is as follows: coherence with fiscal principles is weak, harmful precedent for tax discipline.

Short-term revenue impact is positive, but temporary. Moral hazard risk is very high. Alignment with EU practices shows clear mismatch with transparency & control standards. Impact on formalization is negative – legalizes existing informality. Transparency & fairness is compromised by audit exclusion. Role of tax administration is reduced and ineffective in real oversight.

The “Fiscal Peace Agreement” draft law does not create real peace—it offers a temporary truce with tax evasion. Instead of strengthening voluntary compliance culture, it legalizes avoidance and weakens fiscal institutions.

If passed in this form, it will mark a step backward toward a fair, transparent, and EU-aligned system.

What do you think?

Should we prioritize justice or quick gains? Leave your comments below and share this post if you found it useful!

Leave a Reply

You must be logged in to post a comment.