Effect of fiscal policy and administration approach, 2019

Although the growth of the fiscal burden seems to be the easiest way to narrow the budget deficit, this is not true every time. The main argument is that the fiscal burden is planned to increase/decrease at the same time with private investments (foreign and domestic. This planning has led to less budgetary pressure and, on the other size, investors felt more relaxed in returning their investments.

The current level of fiscal burden does not always come from low rates, but in the case of the Western Balkans the impact of low rates translates to a direct consequence of a low leverage. The reason lies in the level of informality, corruption and the tax system still non harmonised with the economy and the market. But fiscal facilities and tax exemptions also have an impact of up to 1-2% of GDP in the region, de facto reducing the fiscal burden of each country, which implements easing and tax-exempt policies.

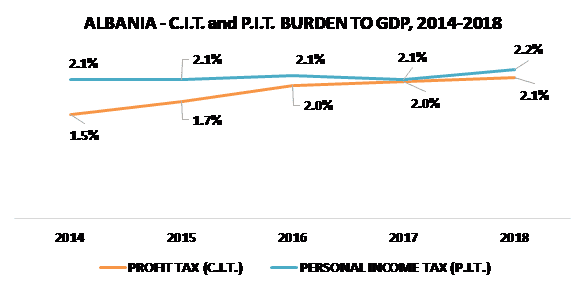

The increase of labour tax burden (personal income tax) and capital tax burden (profit tax) in a progressive approach, mainly on the formal part of the income, is the greatest effect on the fiscal burden that has brought the policy of progressive taxation on personal income and especially the progressivity of tax on wages, besides the total wage relief for unskilled workers with low salaries, which have an impact on increasing the tax base as well as increasing profit from businesses. This fact results when we look at the P.I.T. and C.I.T. revenue trend for the period 2014-2018 with their respective increase by 26.7% and 60.7% (even though half of this increase in C.I.T. goes to the increase of the tax rate in 2014).

The year 2018 is the fourth year of VAT law implementation. This period is considered a period of consolidation of this tax that maintains as much as 35% of total budget revenues. Over the last five years, for certain categories of activities, VAT rates have been reduced to 6% and 10%. The increase in VAT revenues has, however, been up by 18.4%, which corresponds to GDP growth for the last 5 years.

The year 2018, also is the fourth fiscal year for the implementation of the fiscal policy of the tax rates progressivity in Albania oriented to capital and labor taxation although it has in fact been generally applied to wages. Given the results of the collection of personal income tax, we are in condition to monitor its effects on budget performance by understanding the differences between politics and fiscal administration.

The effect of legal changes has had a weak effect on the fight against informality, as the increase in the nominal level of income. More commitment needs to be done to examine the effect of changes deriving from tax competition that compete with the regional one, both for tax rates and customs duties. But what is essential for policy-making is the adaptation of fiscal burden to the performance curve of the economy.

A high level of fiscal burden seems to be difficult to apply in Albania, given that tradition inherited before the 1990s with the burden of 46% to 48% of GDP, the actually burden should now be justified by the shifting burden of future through the application of private-public partnership.

Although these projects are perceived to increase their contribution to the economy, better linkage of regions and lower transport costs, but also greater penetration of technology, there are still many elements that remain unanswered and are not included in transparency regarding the fate of fiscal burden.

In low-productivity economies in the Western Balkans, the lack of more fiscal burden has a negative effect on GDP growth. Reducing the fiscal burden would result in a decline in GDP, as tax incentives for the economy are still considered to have a share-bearing effect on capital and domestic market development.

Populist offers for lowering the tax rates of some WB politicians, where the most pronounced this spirit is to Albanians with statements that are made for the purpose of boosting the economy and investment have resulted in economic and social reality as unreal and regressive in view of the announced objectives.

These unhelpful political offers and support to the economic reality of the Balkan countries have reduced economic productivity and capital investments by shaking investors’ confidence. At the same time, the reduction of tax rates, conceived as unrelated to the policies and other reforms undertaken or initiated by governments have generally affected the increase of budget deficits.

Fiscal administration in 2019, both in Albania and in Kosovo, should focus on the segment of high-income individuals.

This taxpayer category is less burdened by taxes in recent decades. Reducing the tax burden should release the middle-income family. Qualified managers and well-paid employees should be the segment for the highest tax rate by actually receiving high payments. The highest tax rate is already in place if an individual’s income reaches 1.8 times higher than the average income.

In order to realize considerable tax relief, the highest tax rate should be only for taxable income above the levels actually considered as income beyond the high wage / average salary ratio of 1.8 times.

It is necessary that the 30,000 ALL paid salary threshold be abolished and other compensatory forms are available for the value of the tax that can be paid for salaries below this level.

Leave a Reply

You must be logged in to post a comment.