Albanian Banking System between Statistical Stability and Accumulated Risks

A Critical Reading of the Bank of Albania’s Financial Stability Report

The latest financial stability report of the Bank of Albania constructs a broadly optimistic narrative regarding the condition of the banking sector and the resilience of the Albanian financial system. At first glance, the main indicators appear to support this approach, as capitalisation levels remain high, non-performing loans have fallen to their lowest level in the past 15 years, deposits and lending continue to expand, while foreign exchange reserves and the fiscal position remain relatively stable. From a technical perspective, the report is built on sound indicators and recognised prudential analysis standards.

However, behind this calm picture lies a more complex reality. Many of the positive indicators appear fragile and highly dependent on the continuation of a favourable macroeconomic environment. The issue is not an immediate crisis, but the gradual accumulation of structural risks that could rapidly amplify in the event of external shocks.

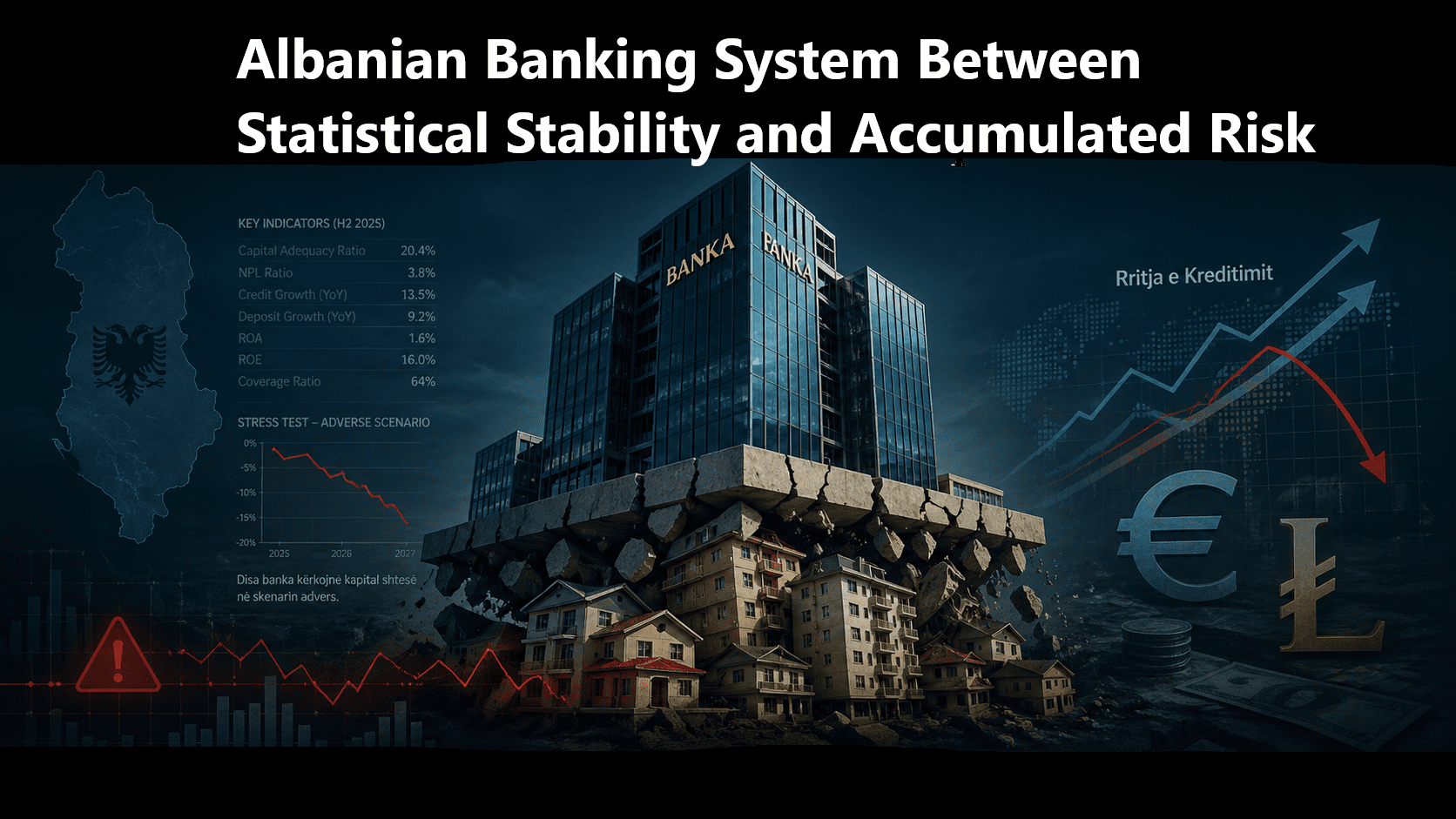

On the one hand, the Albanian banking sector has managed to maintain a high level of capitalisation, with the capital adequacy ratio standing at 20.4%, well above minimum regulatory requirements. Asset quality has also improved significantly, with non-performing loans declining to 3.8%, the lowest level in more than a decade. Credit growth of around 13.5% and deposit expansion of over 9% indicate that the sector continues to benefit from liquidity and public confidence. At the same time, foreign exchange reserves remain at comfortable levels, while the gradual decline of public debt to around 53% of GDP has helped preserve the perception of macroeconomic stability.

Yet behind this statistical stability, several signals are emerging that require much greater attention within the context of monetary and fiscal policy.

Concentration risk in Real Estate

One of the most significant weaknesses of the current system is the growing exposure to the real estate market. Household lending has increased at very high rates, around 20% annually, with the vast majority directed toward housing finance. At the same time, apartment prices, particularly in Tirana and coastal areas, have risen much faster than household incomes or inflation, creating a visible gap between prices and actual affordability.

The Bank of Albania acknowledges the existence of overheating risks but treats them as a “manageable” phenomenon. In reality, the banking system is gradually becoming dependent on a single economic cycle. The collateral underpinning loans depends directly on the continued increase in property prices. Even a modest market correction would reduce collateral values, increase debt servicing burdens for households, already exceeding 30% of income for part of them, and weaken the quality of loan portfolios.

Weaker profitability and deteriorating efficiency

Another warning signal is the gradual decline in banking sector profitability. Net profits have begun to contract. Return indicators, with ROA at 1.6% and ROE at 16%, have entered a downward trajectory, while operational costs have increased significantly and operational efficiency has deteriorated.

This suggests that the expansion of banking activity is becoming increasingly costly and that banks are operating with narrower profit margins. During periods of economic growth, these pressures may remain masked, but in an environment of economic slowdown or higher interest rates, pressure on profitability could intensify considerably.

Declining provisions and underestimated risk

Another development deserving closer attention is the sharp decline in provisioning coverage. Although non-performing loans have fallen to historically low levels, the coverage ratio, around 64% has declined significantly compared to the previous year.

This means banks have built a smaller safety buffer against potential future losses. A realistic interpretation is that the sector is attempting to preserve profitability through lower provisioning costs. In the event of a rapid increase in non-performing loans, the need for additional provisions could directly impact bank capital and significantly weaken balance sheets.

High Liquidity concentrated in Public Debt

System liquidity remains abundant, but a substantial portion has been invested in Albanian government bonds and treasury securities. This creates a strong link between banking stability and public finances.

If the economy faces slower growth, higher financing costs, or fiscal pressures, the banking sector’s exposure to government securities could transmit risk from the public sector into the financial system. This type of interdependence is a classic vulnerability of small and euroised economies.

Stress Tests signal greater vulnerabilities than the official narrative suggests

The stress tests published in the report also provide more serious signals than the way they are officially interpreted. Under the adverse scenario, several systemically important banks would require additional capital. The report describes the impact as “limited”, but this does not reduce the risks faced by individual institutions or the broader perception of systemic stability.

The fact that the sector’s sensitivity has increased compared to the previous year indicates that system resilience is not strengthening at the same pace as risk expansion.

Euroisation and Exchange Rate risk

Another underestimated dimension remains foreign currency exposure. Despite efforts toward de-euroisation, euro-denominated real estate loans continue to represent a significant share of lending. At present, the strong Albanian lek masks this risk.

However, in the event of a sharp exchange rate correction, debt servicing burdens for households and businesses with euro loans would increase immediately, creating direct pressure on loan portfolio quality.

External Shocks could activate internal vulnerabilities

The core critique of the report lies precisely here: the current system functions effectively only as long as the macroeconomic environment remains highly favourable.

If Albania were to face an economic slowdown, geopolitical shocks affecting tourism and remittances, rising energy prices, or a sharp depreciation of the lek, hidden vulnerabilities could rapidly surface.

A weaker economy would undermine the repayment capacity of households and businesses that borrowed at the peak of the property cycle. An energy crisis or regional instability would reduce tourism revenues and consumption, while an exchange rate correction would increase the real burden of euro-denominated debt.

In such a scenario, the combination of rising non-performing loans, falling collateral values, and the need for additional provisions could quickly erode existing capital buffers and create serious liquidity or capital problems for certain banks.

The debate on financial stability in Albania is therefore no longer limited to capital adequacy levels or declining non-performing loans, but rather concerns the quality of the current growth cycle and the way risks are accumulating within the banking system.

Recent developments indicate that the banking sector is becoming increasingly exposed to the real estate market. Rapid growth in mortgage lending and rising property prices have created a less diversified risk structure, where financial stability is closely tied to the continuation of the current real estate cycle and the preservation of favourable macroeconomic conditions.

In this context, macroprudential standards are becoming important not only as technical supervisory instruments, but also as indicators of the quality of financial expansion. The discussion surrounding LTV and DSTI ratios is directly linked to whether credit growth is based on real repayment capacity or optimistic expectations regarding the property market.

Equally significant is the gradual decline in provisioning during a period of rapid credit expansion. This suggests that the sector is operating under a relatively benign perception of risk, reducing the resilience of balance sheets to future shocks.

Another critical dimension remains sectoral credit concentration. In economies with limited investment alternatives, the massive allocation of capital toward real estate creates a self-reinforcing cycle: rising prices generate more credit, while expanding credit fuels further price increases. This makes the system increasingly vulnerable to market corrections.

At the same time, the real quality of collateral remains one of the least transparent elements of the system. During expansionary periods, property valuations are often influenced by optimistic expectations, creating a gap between the nominal value of assets and their actual capacity to absorb losses.

The Albanian banking system remains capitalised and liquid for now, but the nature of its stability appears more cyclical than structural. Rising exposure to real estate, declining provisions, weakening profitability, and dependence on a favourable macroeconomic environment suggest that the system is gaining stability in appearance while becoming more fragile in structure.

In this context, the optimistic tone of the report reflects current statistical stability, but not necessarily the system’s long-term resilience against potential economic or financial shocks.

Leave a Reply

You must be logged in to post a comment.