Tax Burden in the Western Balkans in 2022

According to Report about Tax Burden 2022 from ALTAX, in 2022, on average in the Western Balkans region, governments generated revenues to the extent of 34.8% of GDP. This represents a percentage like the level raised in OECD countries (37.5%), but lower than the average of EU countries (45.2%). Moreover, the trends differ on average between the EU and the Western Balkans: compared to 2008, there was a decrease of 1.2 p.p. in the Western Balkans and an increase of 1.4 p.p. in the EU [1].

The budget revenues in BP6 in 2022 have been a function of the programs and reforms undertaken with a comprehensive goal of promoting economic growth, encouraging, and increasing employment, improving the quality of the macroeconomic environment, and increasing the penetration of innovation in function of improving services for citizens, as well as filling gaps of various natures in the journey to be integrated into the European Union.

Tax burden according to tax rates

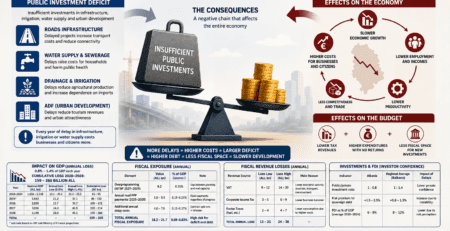

Economies in BP6 have a small tax base for incremental revenue generation, indicating low potential for economic expansion and low gross fixed capital formation, although expanding in recent years[2].

Such a challenging situation hampers the capacity of governments to promote inclusive growth. Investments in digital technology are bringing a new wave of digitization to the region, driving the development of new means of revenue collection, especially taxes.

But what is needed is a larger income base, which enables the expansion of services for the population, and a difficult challenge is the timely implementation of the relevant reforms that governments have promised over the years.

While investments may be on the rise, they face the challenge of increasing revenue collection at the same rate as spending.

High food and energy prices contributed to the increase in tax revenues throughout 2022, but this increase, which should have come from better distribution of the fiscal burden through the expansion of tax bases, made administrations even more lazy by felt accommodated with meeting the rising income level.

Tax revenues in 2022 mark the level of 31.5% of BP6 GDP. In the tendency to align every possible fiscal aspect with a positive approach to improving budgetary health, there is still an obvious gap.

According to the indicators also presented in the Report, in 2022 we see the highest tax burden in Serbia with a collection level of 38.7% of the country’s GDP. However, this year, Bosnia-Herzegovina has increased its collections more, which holds the second place for the highest tax burden at 37.4% of the country’s GDP. In third place is Montenegro with the tax burden at the level of 34.3% of the local GDP. These three BP6 countries have a high fiscal burden on average for the last 5 years, 2018-2022 and according to the graphic presentation above.

Performance at high levels comes from both a more expanded tax base, but also a better level of administration, as well as a higher level of administrative capacity and vision closely linked to economic reality by limiting tax exemptions and the entry of investments that have significantly increased the fiscal contribution to the countries’ budgets.

All three of these countries have a level of fiscal burden above the BP6 average, but significantly higher than other BP6 countries by at least 14% more based on the 5-year average.

The second group of BP6 countries, North Macedonia. Albania and Kosovo, and have a fiscal burden of 27.2%, 26.3% and 25.2% of the respective GDP of each country. According to the ranking above is also their positioning in BP6, respectively in fourth, fifth and last place.

The comparison of fiscal burdens also explains the elasticity of the distribution of the main part of the countries’ budget expenditures based on their own sources of income.

The burden of VAT in BP6 holds about 36.6% of the total tax revenues still shows a problem of the tax base for other taxes, which must be addressed for the diversification of the income pyramid. Kosovo bears the largest share of VAT, followed by Bosnia-Herzegovina (VAT and Excise are set in the graph), a fact that shows the great dependence of budgets in these countries on consumption and imports. While other countries also have high levels of VAT in the structure of budget revenues, they still have a better diversification of sources of income from direct taxes and other taxes.

The latter also has a high burden for labor taxes, making the fiscal burden high. Kosovo is still far from the administration close to the potentials of labor taxes and shifting the burden of VAT towards the burden of income tax. Meanwhile, efforts to shift the burden should be gradual and without affecting the tax base.

For example, in Kosovo, where the reductions-increases of VAT rates have brought as a secondary effect claims of other sectors not included in the benefits from the reduction, to also seek those benefits from the fluctuating policy and contradictory to the principles of VAT, where the policy of exceptions or escalations is not tolerated.

Another case comes from Albania, where the taxing policy of farmers is changed by changing the VAT refund scheme for raw materials, or the change in the policy for packaging taxes, which bring effects to the destruction of the credibility of the scheme and the reduction of the level of compliance. voluntary enforcement of the law by taxpayers.

If we look at the performance of direct taxes, in 2022, their burden is 15.5% of total tax revenues in BP6. Albania, Serbia, and Montenegro are the three countries that tax income from work more than the others. Meanwhile, the other countries of BP6 have levels that show taxation below the capacities, which has relevant specifics in Bosnia-Herzegovina, compared to Kosovo and North Macedonia.

If we look at the work burdened with the payment of social and health contributions, we can see that the highest work burden is in Serbia, Bosnia-Herzegovina, and North Macedonia. In Albania, Montenegro and Kosovo, the contribution burden has minor impact on fiscal productivity, although Kosovo implements a private scheme of mandatory private contributions.

The policy of low burden on insurance contributions in Albania, Kosovo and North Macedonia is uncompetitive compared to their neighboring countries. But it also does not create opportunities for the budget to spend more on social funds, a fact that was noticed more in Albania and Kosovo. Meanwhile, the M. of the North has switched to a more flexible scheme of compulsory private pensions, which helped the country’s budget, not exerting the pressure it had in Albania and less so in Kosovo for increased social costs.

Capital gains tax is the tax an investor must pay when an investment is sold. This tax is a tax liability for the tax year in which the investment is sold.

Long-term capital gains tax rates for tax years 2022 and 2023 are 10%, 15% as standard rates. Meanwhile, reduced rates of profit tax apply at the reduced limits of 3%, 5%, 9%, 12%

The burden of taxes on capital is at low and approximate levels among BP6 countries and in the best case it is as much as 2.9% of the GDP of Serbia or as much as 2.3% of the GDP of Albania.

Other countries register a level below 2% of local GDP, as an indicator that shows various stages of capital circulation, but also opportunities to increase the tax base and collections from this important tax that also shows the level of effectiveness of foreign and domestic investments.

[1] https://www.oecd-ilibrary.org/sites/2bf55d60-en/index.html?itemId=/content/component/2bf55d60-en

[2] https://www.imf.org/-/media/Files/Publications/WP/2023/English/wpiea2023031-print-pdf.ashx

Leave a Reply

You must be logged in to post a comment.