Fiscal burden in countries with progressive taxation and those with flat taxation

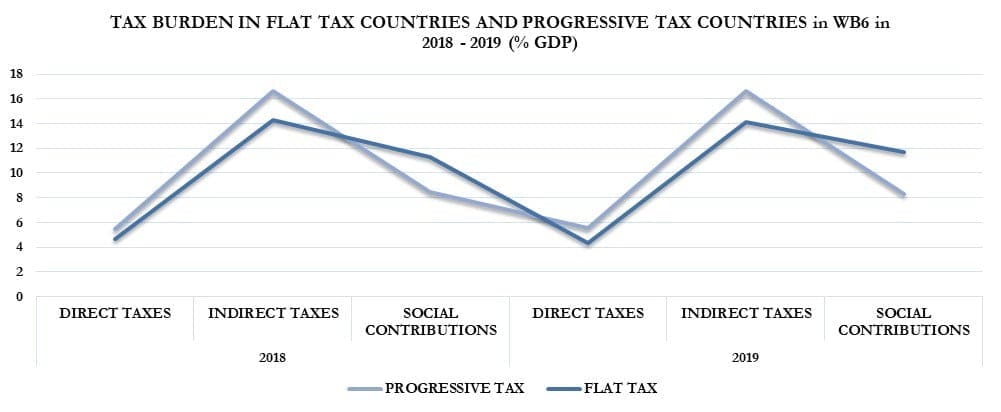

Fiscal revenues from WB6 countries applying progressive taxation (Montenegro, Kosovo, Albania, Serbia) compared to countries implementing flat taxation (North Macedonia, Bosnia and Herzegovina) have a higher burden, respectively of 1.8% and 2.1% of GDP in 2018 and 2019.

The taxation model for capital and personal income is seen to be unrelated to the burden of insurance contributions, or even indirect taxes.

Albania and, in part, Montenegro and Serbia (as of 2019) apply a progressive personal income tax system, which still carries with it a sharp and yet unaddressed problem for solutions related to the expansion of the narrow tax base on capital and labor. The Balkans have been characterized by fiscal policies that have focused on stabilizing the profit tax rate, a tendency to adapt to progressive taxation on personal income, and a slight reduction in the rate of social contributions.

Countries implementing progressive taxation have an average contribution burden for 2018 lower than countries implementing flat taxation with 2.7% less and for 2019 it is 3.4% less. But this difference is a result of the high level of fiscal burden in Bosnia and Herzegovina. This fact seems to affect the average fiscal burden from social contributions and is the same reason for the average tax burden on indirect taxation in countries with progressive taxation, which are 2.3% and 2.4% above 2.4% and 2018, respectively other WB6 countries with direct flat taxation regime.

Comparing the level of fiscal burden for direct taxes in the Western Balkans with the EU-28 average, the difference is more than double.

This fact between comparisons for the same model, on the one hand comparing fiscal policies through tax rates, while comparing fiscal burdens on the other, shows once again that the administration is still working below the capacity provided by fiscal legislation in the respective states, which implies, inter alia, the presence high tax evasion.

In the total fiscal burden, it appears that countries with low productivity in the collections of a constituent group of total fiscal burden (eg insurance, and other taxes in Kosovo) are offset by higher receipts from another constituent group (Indirect Taxes in Kosovo).

The various studies conducted on informality in the labor market in the Balkans show the concern of a labor market informality that is changing and decreasing at a slower pace than the forecasts and programs of the Balkan governments. A narrow base of direct taxes still shows a still-closed transition in terms of the greater contribution that direct taxes on capital and labor income (companies and individuals) have to budget.

All Western Balkan countries apply a flat rate of profit tax, except for Albania and Kosovo.

Leave a Reply

You must be logged in to post a comment.