Distribution of fiscal burden according to the budget destination in Kosovo

Impact of new measures to improve the business environment, facilitation of imports for the manufacturing sector, exemption from customs duties in the case of imports of technological equipment, plans to narrow the tax gap and informal economy, measures for advancing the efficiency of revenue collection by collection agencies, with a particular focus on reducing debt stock, etc. are considered to have the potential to increase the level of revenue.

Notwithstanding this, for reasons of cost planning on the basis of stable income, a conservative approach has been applied in assessing the impact of these measures. Consequently, expenditures can be maintained at a manageable level, and with the aim that expenditure commitments are based on sustainable funding.

To build trust in a fiscal system that works to increase the well-being of its citizens, an analysis needs to be made of the return of taxes paid as a fiscal burden on public spending on taxpayers.

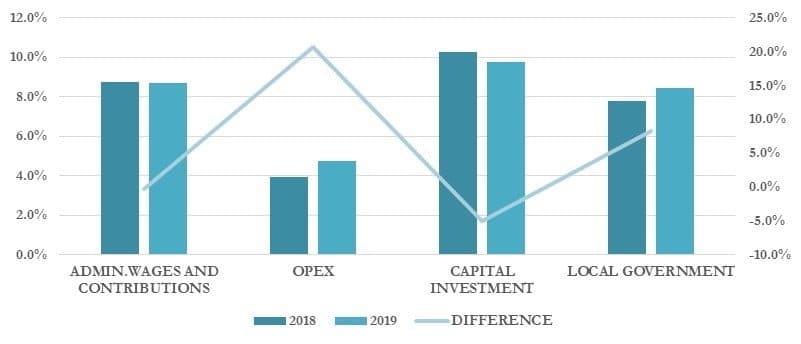

In the analysis of budget expenditures for the last 2 years, according to table 35 it is seen that total expenditures in 2019 have an average annual increase of 7.3% year on year, with an increase in absolute value by 142 million Euros. Meanwhile, revenues increased on average year by year by 6.3% with a change in absolute value of 98 million Euros.

The largest increase in total costs is borne by operating and maintenance costs (goods and services) with a change of year by year by 17.6%, or as much as of 0.8% of GDP. In absolute terms, this change is worth € 44 million. One of the factors influencing the growth of this category is the reclassification of expenditures from the category of capital expenditures to the category of goods and services.

Capital expenditures are unchanged, but in respect of GDP they show a decrease of 0.6%, or a change from year to year with less than 5.1%. However, capital expenditures have had the highest rates at 69% in 5 years. An important part of the capital investments is the continuation of the M2 project for Mitrovica, and other investments for the improvement of local, sports and educational infrastructure, and projects which, compared to last year, have marked a significant increase.

Wage and social contribution expenses (administration) have increased in absolute value by 24 million Euros with a change of 4% year by year. Wage and bonus costs continue to account for a significant share of total spending.

Expenditures for the local budget and transfers have a positive change of 12.4% year by year, with an increase in absolute value of 69 million Euros. This increase in transfer subsidies includes the implementation of the Teachers’ Law and the natural increase in the number of pension beneficiaries.

Expenditures for capital investments in 2019 account for 25.3% of total expenditures and in 2018 they are as much as 27.2% of total expenditures.

Administration costs account for 29.4% of total expenditures. In 2018, their share is 30.3% of total expenditures.

Expenditures on transfers for local government account for 29.9% of total expenditures, while in 2018 they accounted for 28.6% of total expenditures in 2014 and 2018.

Comparing the tax revenues with the budget expenditures, which coincide with them, it can be seen that the revenues from the personal income tax justify only 25% of the budget expenditures for the salaries of the state administration. Meanwhile, only 19% of corporate income tax revenues and property taxes together are justified for capital investment expenditures.

Other destination budget expenditures (for local government and operating expenditures), together with the completion of parts not covered by capital expenditures and wages, are covered by indirect taxes, which meanwhile go to other local expenditures.

Leave a Reply

You must be logged in to post a comment.